Looking to purchase small business insurance? Is it time to renew your policy? Just what can you expect from the insurance process, and why should you care?

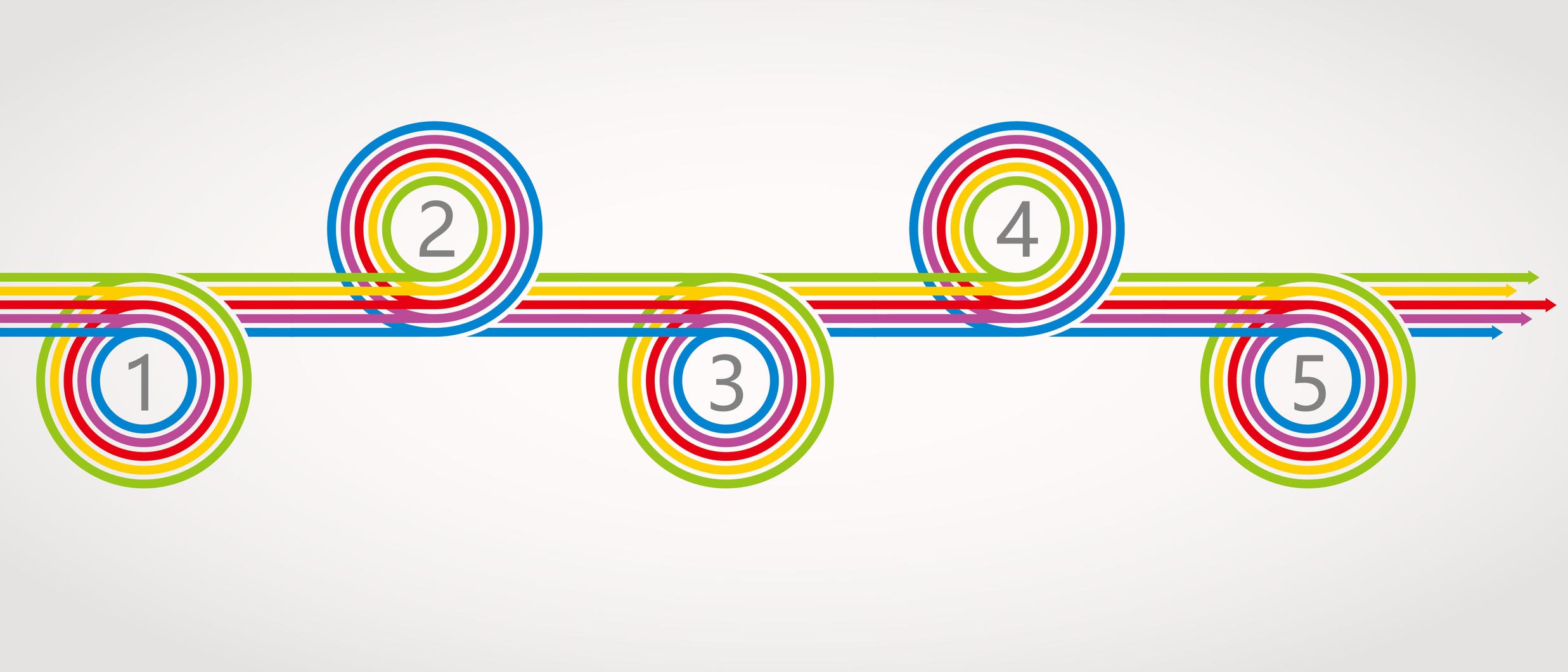

Finding the right business insurance can seem overwhelming at first — and also in the weeks, months, and years ahead when you need to revisit your terms or renew your policy. Understanding the key steps and touchpoints — from getting a quote to filing a claim and renewal — can help you get the support you need from your broker and your insurer, right from the start and at any point in the future. Here’s some helpful information on the key steps in the insurance process, so you know what you’re getting into.

1. The quote

This is where it all begins. Your quote will give you a good idea of the premium you can expect to pay, but getting a quote is about more than just price. A small business insurance policy can offer a spectrum of coverages to protect different aspects of your business — learn which ones might apply to your unique operation, instead of choosing blindly.

Your broker should help you understand the risks your business faces and which insurance features could meet your specific needs. They should also compare different available products to identify any potential gaps and determine which one is a best fit for your business.

A small business insurance policy can offer a spectrum of coverages — learn which ones might apply to your unique operation, instead of choosing blindly.

2. Risk assessment

Property risk may be the first business risk that comes to mind; most businesses rely on specific and sometimes very expensive equipment, tools, and other physical property to get the job done. But that’s not all you need to worry about.

Of course you want to protect your business from incidents like fire or flood that could put your property in peril, but have you also considered how you would shelter the storm if a customer took legal action against your business? Or what would happen if a natural disaster sidelined your business operations for several months?

This is where you broker’s expertise comes in: they’ll be able to help you understand other (perhaps less evident) exposures, like workplace safety, liability, and cyber risk. The more thorough your risk assessment is when you begin your policy, the more peace of mind you can enjoy when it comes to protecting what really matters — and avoiding nasty surprises.

3. Ongoing monitoring

So, you’ve got your policy in place and all your bases covered. Time to sit back and forget about it, right? Not so fast — your business is always changing, morphing, and growing, and so should your insurance and risk management strategy.

Think of your insurance broker as your business partner: as your business grows, a good broker will be proactive with recommendations to align your coverage with your changing exposures, and keep your best interests in mind when suggesting changes. For example, if your company is expanding and hiring new employees, you may face new human resources concerns or questions about contracts. It will be much better to sort those questions out now and avoid a misstep that could land you in a wrongful dismissal lawsuit.

Think of your insurance broker as your business partner: as your business grows, a good broker will be proactive with recommendations to align your coverage with your changing exposures.

4. Claims

Just thinking about making a claim can be enough to cause a headache, but consider it this way: a claim is the first crucial step to restoring your business after a loss. The claims part of the insurance process can be complicated and timelines may vary, which can lead to stress and worry as you continue in your recovery effort. Fortunately, sound knowledge can help alleviate that emotional hardship — get to know the 5 steps of the insurance claims process now so you can proceed quickly and confidently if you ever need to file a claim.

As is the case with any response, communication is important while you’re going through the claims process. Your broker and insurer should be in constant communication with you throughout the process to keep you informed, and you should feel comfortable reaching out to them for answers or clarification along the way. They can also point you toward other valuable services that can get you back to business (and back to your old self) after the traumatic event.

5. Renewing

When renewal time comes, you can count on a call from your broker. This is a great time to have an in-depth discussion about your business, reviewing the last year of your operations and looking at parts of your business that many have changed. Now you can decide whether to adopt some new coverages and limits that will meet the needs of your business for the year ahead.

However, there may be reason to revise your policy before renewal. Have you gone through a major change? Even a minor change could be cause for a closer look at the terms of your policy. You don’t have to be continually connecting with your insurer or re-reading the fine print, but don’t be content to stand on the sidelines, either. Regular check-ins can only help in the long run.

Working with the right partner

Looking for the right insurance broker for your small business? You’ve come to the right place: Northbridge has an outstanding network of reputable brokers at the ready. Let us help you get the right quote for your business with the help of a broker near you.